We also have a credit card with 2-day payment, combining the best of debit and credit. The 2-day payment lets you buy on credit while shortening the settlement period to 48 hours. This way, everything you spend is reflected in your card transactions right away, but it is debited from the associated account in 48 hours. This payment method lets you recover your card's credit limit quickly so you can continue your day-to-day purchases.

This will be the default payment method for cards with 2-day payment (such as Visa &Pay and Visa MyCard).

You also have the option to customise the payment day and instead of paying the credit in 48h, paying it weekly, monthly or as often as you specify (example: once you have spent €200). You will not have to pay interest in any of these cases, since you will return the full amount of the credit drawn down at the end of the agreed settlement period.

This card also lets you use the balance in your account (up to €3,000) once you use up your credit, as long as the associated account where you have the balance is with CaixaBank, and you have sufficient balance to cover both the credit limit you have used up and anything you want to spend over that limit.

Here's an example: Juan uses the card with 2-day payment for everyday purchases. On 10 April, he uses the card to pay €12 for the transport card, on 11 April he spends €6.90 on a salad and on 15 April €25.90 at the supermarket. Juan will see each of these card transactions in the app or CaixaBank Now as soon as they are made, and has to pay back the credit used, with no interest, as follows: €12 on 12 April, €6.90 on 13 April and €25.90 on 17 April.

And an example to understand how to use the balance in the account in addition to using the credit: Juan has a balance of €200 in his CaixaBank account associated with the card, and the credit limit on the card is €100. If he needs to make a purchase for €150, he can do so because he will charge €100 to his card (which he will pay in 48h) and €50 will be paid directly from his account balance at the time of purchase.

The card also allows other payment methods that you must expressly request, such as deferred payment of all the credit you have on a monthly basis, or payment in instalments of a certain transaction or purchase. These two payment methods do require interest payments, which are specified both in the pre-contractual information (INE) and in the contract.

A deferred payment consists of paying back the credit you spend gradually, instead of paying the total amount at the end of the agreed settlement period. This way, you decide what monthly instalment you want to make to pay back the credit used. Even if you use more credit each month than the chosen instalment, you will only pay the chosen instalment, provided that the amount paid back is the minimum specified by CaixaBank Payments & Consumer to ensure your debt is repaid in a timely manner. When choosing the level of the monthly instalment you want to pay, bear in mind that the higher the monthly instalment you pay, the lower the total cost of the credit to be repaid, because you will repay the loaned credit sooner.

Paying in instalments consists of paying for a certain purchase or transaction on credit and instead of paying it all back at the end of the month interest-free, you pay it off over however many months you decide, including the associated interest or a fixed fee, also reflected in the contract.

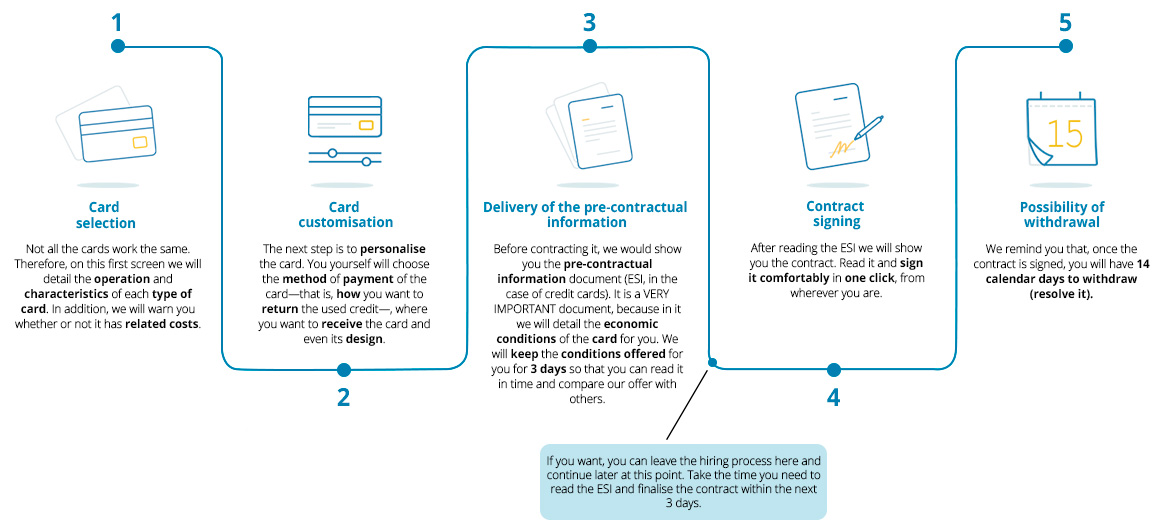

To be as transparent as possible with you and to let you know how our 2-day payment card works before you even start the application process, we provide you with an example of the pre-contractual information document (INE) and an example of the contract, which we attach below.

PLEASE NOTE: the NIR and APR numbers that you will see in both the INE example and the sample contract are specific to the EXAMPLE and therefore may not be those that we will apply to your card, as these conditions in the examples are the maximum applicable. We provide the maximum values for these numbers because, as you have not started the contracting process, we have not been able to study your financial situation, so we cannot tell you in advance what financial conditions you will have on your card. For this reason, we prefer to show you the maximum rates.

The maintenance fee for the Visa&Pay and MyCard is €48.